Open Brief aan Wereldhave (update)

20 februari 2020 - 07:00u

Update 19 februari, 17:00

Wereldhave heeft direct gerageerd op onderstaande open brief door de IEX-forumleden. De ondertekenaars krijgen een uitnodiging om te komen praten en de voorstellen worden 'bestudeerd'.

De volledige tekst van de reactie, ook hier te lezen:

Wereldhave appreciates initiative by The Third Way-investors and will extend invitation for a meeting

Corporate update 19 February 2020

Wereldhave has been approached by a group of investors who call themselves The Third Way through the web-based platform IEX.nl, with an alternative way to execute the LifeCentral strategy.

The Boards of Wereldhave appreciate the initiative to think along with management and present an adjusted route to sustainable growth for Wereldhave. We welcome the fact that this alternative plan is largely based on our recently presented LifeCentral strategy.

We do want to emphasize that in our current talks with our institutional investors we experience general support for the LifeCentral approach, whereby investors rightfully note that the strategy is challenging, but viable and feasible and ultimately beneficiary to all stakeholders including shareholders.

Wereldhave will carefully study the proposals by The Third Way in the next weeks and will extend an invitation to the group to meet and exchange views and ideas about our LifeCentral strategy and their proposed alterations.

We blijven een en ander uiteraard op de voet volgen bij IEX.

Open brief aan Wereldhave

Aandeelhouders op het IEX-forum presenteren een alternatieve strategie voor het vastgoedfonds. Inzet: 120% rendement in twee jaar.

Een groep beleggers, samengekomen op het IEX-forum, schrijft een open brief aan de aandeelhouders en commissarissen van Wereldhave.

Hun boodschap: de ingezette nieuwe strategie 'LifeCentral' van Wereldhave creëert te weinig waarde en verhoogt de risico's. In de brief stelt de groep van 19 aandeelhouders een aanpassing van de strategie voor, die ze '20-20 Vison LifeCentral' noemen.

In het kort: de aandeelhouders willen dat Wereldhave meer assets gaat verkopen dan het nu van plan is, en ze willen Wereldhave omvormen tot een 'asset light'-vastgoedpartij die zich nog meer dan in de huidige strategie op een beperkt aantal activiteiten richt. Door de verkoopopbrengsten deels uit te keren aan aandeelhouders kunnen die over twee jaar een rendement van 120% tegemoet zien.

Opvallend, want de nieuwe strategie van topman Matthijs Storm werd al gezien als een harde ingreep en een breuk met het verleden. De beleggers op het Wereldhave-forum vinden de plannen niet ver genoeg gaan en te weinig concrete vooruitzichten schetsen. Hun alternatieve plan schetsen ze in de open brief, die we hieronder volledig publiceren. We zullen Wereldhave uiteraard om een reactie vragen.

IEX forum WH

February 14, 2020

To: RvC Wereldhave RvB and shareholders Wereldhave

Subject: 20-20 Vision LifeCentral

Dear sirs,

As a group of shareholders of Wereldhave we are not only worried about the future of WH but propose a concrete plan of action to improve the LifeCentral strategy with a 20-20 Vision. We would like to invite you to engage in direct and concrete dialogue with us through IEX initially, to the benefit of all stakeholders.

1. Executive Summary

In essence, LifeCentral is about the future of selected Dutch malls. Management proposes to invest there the net proceeds of the sale of French malls – around €350 mln. That generates a ROE of 5% overall and surprisingly only 3% in the Netherlands - where the investments are to be made. These are already sub par returns and additionally should be placed in the context of the CEO’s statement that the industry is evolving and WH should be judged as a ‘normal company’ – thus with a much higher cost of capital going forward.

Moreover, the execution focus isn’t well defined as Moody’s stated in its downgrade. Investment analysts struggle with the lack of specificity. As current shareholders, we feel necessitated to address you directly with a request to engage on more concrete and far reaching strategy action.

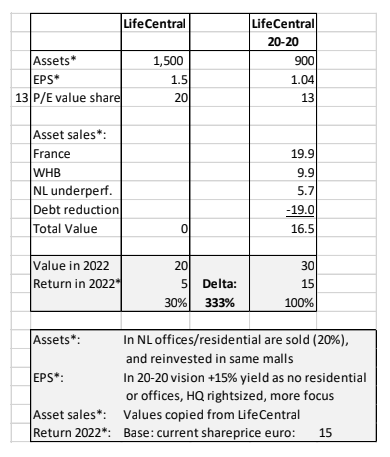

Our Vision 20-20 is to improve LifeCentral: sell French, non-core and additionally Belgian assets and thus return within two years 110% of share price – currently €15 – to shareholders. The investments in Dutch malls would be funded by the sale proceeds of their 20% of m2 intended for – in our opinion non-core - offices and residential.

Not only is this a healthy ratio, but it ensures focus and accountability at mall level. Sadly the reality is that both the original LifeCentral and our added 20-20 Vision lead to a shrinking of m2 at the expense of shareholders. But ours adds tremendous value immediately, thus reduces execution risks and ensures focus and accountability.

It tunnel-focuses on the longevity of the critical LifeCentral concept i.e. Wereldhave afterwards. And it dramatically improves shareholder returns overall, both short and long term. Please see table below, a summary of our proposal vs. the LifeCentral strategy:

2. Geography

France

- We agree with the phased sale of all assets. The EPRA NIY of 4.6% matches the recent URW transaction so:

- KPI: sale at bookvalue e800 mln in 2020-2022 (as proposed by LifeCentral).

Belgium

- As WHB has no material synergies with NL, has a great market valuation at NAV, much higher NIY (lower Cost of Capital), a lower finance cost and a much lower LTV coupled with easy access to financial markets, thanks to stock listing the 66% shareholding should be sold in 2020.

- KPI: sale at current shareprice, or NAV, at e400 mln in 2020

Netherlands

- Selling above F&WHB and Dutch underperformers will allow the LifeCentral vision to be focused on just a single digit number of Dutch centers, as proposed by Mr. Storm.

- KPI: sale non-core, implement LifeCentral in 2020-2023.

Headquarters

- Given the above reduction a right-sizing can take place. Additionally and importantly, location can be shifted from expensive (500 e/m2) Schiphol to a LifeCentral location (now 188 e/m2) thanks to its mixed use. This will reduce costs (for HQ), increase revenues (occupancy on location) while allowing HQ staff to have ‘feet on the floor’.

- KPI: As soon as possible relocate HQ to a LifeCentral center

3. LifeCentral: a deeper dive financially

Currently the NL rents are amongst lowest in the market and occupancy stands at 95% (temporarily down due to Hudson Bay). LifeCentral views to:

- decrease m2 by exactly the vacancy percentage, and additionally

- allocate 20% to residential/offices,

- allocate additional 5% to F&B,

- allocate undefined but significant additional % to entertainment,

- allocate additional 18% to health etc.

→ result: current tenants go from 95% to 40% of m2.

It is thus clear that immediately there will be a significant upward pressure on rents from current tenants based on halving of space and attractiveness of LifeCentral vision.

The LifeCentral strategy views to own the offices and residential spaces created. In line with the pre-Storm strategy, we view these activities as non-core. Moreover, we believe, based on calculations outlined in the LifeCentral presentation, that the proceeds of the sale of this non-core business (20% of current m2) should more than suffice to fund the LifeCentral capex for the core 80% of space.

N.B.: In the unlikely event there would be temporary cash mismatches between sale (while upfront) and modernization capex, the refined per location plan to be worked out should highlight these.

KPI: Our Vision 20-20 thus foresees:

- a finance plan per location that should be cash / CAPEX neutral or positive for WH.

- based on input per location a timetable can be established. From the presentation we are under the impression most could be done before 2022.

4. Making LifeCentral sustainable

Based on the almost existential success of the above and the LifeCentral concept, in 2022 at the end of his current term Mr. Storm would be offered an additional four years. His mission would be to separate the physical centers from the asset and operational management (i.e. his vision: the LifeCentral added value).

The physical assets could be sold to investors at much lower NIY than current, thus realizing a tremendous uplift for shareholders - thanks to LifeCentral.

The new WH would thus be asset light and can focus fully on marketing its added value LifeCentral to the wide market of asset owners. Significant economies of scale cq. commercial margins can thus be achieved. This is in line with current standard practice in the hotel industry and allows WH to capture an oversized percentage of the margin.

5. Shareholder returns

Currently WH is trading at €15, grossly undervalued compared to NAV. The old LifeCentral strategy targets an EPS of 1.5, thus not providing much of an uplift.

The current discount for NL is even 80% after deducting France and WHB (see below). In 2022 when all non-core assets have been sold, and LifeCentral capex has been invested - but the NL assets (currently valued at e900 mln) are still owned - we would strive for a conservative LTV of 35% of current low valuations. This would allow sufficient headroom for fluctuations (to be confirmed by LifeCentral plans per center). Remaining debt would thus be e320 mln.

The benefits of the ‘refined LifeCentral’ strategy

Sale France: €800 mln Sale

WHB: €400 mln Sale

Dutch underperformers: €230 mln

Total proceeds: €1.430 mln

After deducting the €200 mln debt owed by WHB, the current debt stands at €1.1 bln. To reach the desired 35% LTV or €320 mln, €780 mln of the proceeds will thus be used to repay debt. The excess liquidity of e650 mln can now be distributed to shareholders as a superdividend or buy-back, representing as much as €16+ per share: a 100% return!

Including dividends the shareholders thus stand to earn 120% over he next two years, depending on speed of execution. The new WH would be worth €10 per share at current low taxation valuation with EPRA NIY of 6.8%, and potentially the current valuation of €15 if well implemented and EPRA NIY at around market rate of 4.5%.

We suggest you compare the above returns to shareholders to the existing strategy, the difference is baffling. In our opinion it leaves WH no choice but to consider it through a deep dive, to be presented to you and to be reported to shareholders.

While LifeCentral currently has an open-end – as explained doubted by many stakeholders -, by adding our Vision 20-20 the upside is protected through the sale of French assets and WHB, while the likelihood of sustainable long term success is amplified.

6. Financial execution

We propose to appoint an accountable person dedicated to the asset sales in phase 1 and 2. From the above it is clear that this would be a tremendous step forward. Additionally, the benefit is that the going concern WH can now focus 20-20 on its future: LifeCentral.

Sincerely yours,

The Third Way…

Input appendix: Nya

Signatories:

- Aloys M. Bahos

- Andre Brasser

- Cok Verduijn

- Henk Wijnalda

- Henk Sloot

- Jan Oorsprong

- Jan van Putten

- Joop Bakker

- Klaas Klaver

- Marcel Blom

- Martijn Blok

- Rob Molenaar

- Roel Oldeman

- Steffen Thijs

- Toon Ruizendaal

- Wilco Schouten

- Willem Achterberg

- Willem van Rossum

- Wim Vink

APPENDIX: ROE calculation LifeCentral

One of the most important questions to ask ourselves as shareholders is the following: what are we getting for the €300-350 mln (roughly €8 per share) that management is planning to spend on redevelopment CAPEX for the Dutch operations? In other words, what is the total ROE on the Dutch part of Wereldhave given the above mentioned investment CAPEX?

In order to calculate the ROE we use management’s guidance for the direct result of €1.50 per share, or about €60 mln in total, assuming 40.3 mln shares of Wereldhave outstanding. Of this total of €60 mln in direct result about €30 mln is generated by Wereldhave’s 66% stake in Wereldhave Belgium. This €30 mln corresponds to 2/3 of Wereldhave Belgium’s direct result of €45 mln as was reported by the Belgian company for FY 2019.

So what we are left with now is €30 mln of direct result coming from the Dutch operations. As per the original LifeCentral plan this €30 mln will be generated by €900 mln of Dutch assets. Now assuming that the LTV will have been lowered to 35% by the assets sales as described in Wereldhave’s FY 2019 press release, this implies that €30 mln in direct results has been generated by circa €590 mln of equity in Dutch assets.

Knowing this amount we are able to calculate the ROE for the Dutch assets by straightforward division resulting in a ROE of 5%. However, we are forgetting something in this calculation, namely the extra CAPEX of, let’s say €350 mln of redevelopment CAPEX. By adding this amount to the €590 mln of Dutch equity we ultimately obtain a much lower ROE, namely 3.2%.

Calculated differently, when subtracting the FY 2019 66% equity of WHB from the group we obtain €865 of equity invested in NL. The €30 direct profit thus indeed represents more or less same, 3.4% ROE (0.2% difference explained by 35% LTV assumption in first calculation). This below hurdle return of 3.3% will only be realized if every aspect of the original LifeCentral strategy is executed exactly as planned (or better) as there is little, actually no room, for mistakes on part of the management.

Based on the conservative calculations presented above we, the shareholders, believe that the decision to allocate €300-350 mln in precious shareholder capital to redevelopment of Dutch assets for such a low return on Dutch equity, while leaving no room for error, is a grave misallocation of said capital.

Moreover, the inferiority of this capital allocation decision should be obvious in the light of other capital allocation opportunities that create not only extraordinary, but also more certain amounts of shareholder value, either directly in the form of cash dividend to shareholders, or indirectly through share buybacks. Especially the latter will, when implemented in significant amounts lead to enormous creation of shareholder value given the current dramatically depressed share prices of Wereldhave.

N.B.: A final comment is on the relationship with WHB, a separate stock-listed company. Out of the above follows that in the original LifeCentral plan WH would own 66% of an entity that is not only much more profitable with a ROE of 6.6%, but also 50% larger in terms of profitability. From many angles we don’t think this is ideal.

De Redactie van IEX bestaat uit een team van content managers, journalisten en analisten, met opgeteld meer dan honderd jaar ervaring in het produceren en publiceren van beleggingsinformatie en -opinies. De informatie in deze column is niet bedoeld als professioneel beleggingsadvies, of als aanbeveling tot het doen van bepaalde beleggingen. Het is mogelijk dat redactieleden posities hebben in een of meer van de genoemde fondsen.